Funding the Plans

- Featured Image

-

The ATRF Board has established a funding policy that provides a framework for the sound financial management of the plans. The overall objective is the sustainability of the plans—to ensure the plans will be able to pay the pensions earned by members today and over the long term at a cost and risk acceptable to the plan sponsors.

Plan Funding Status

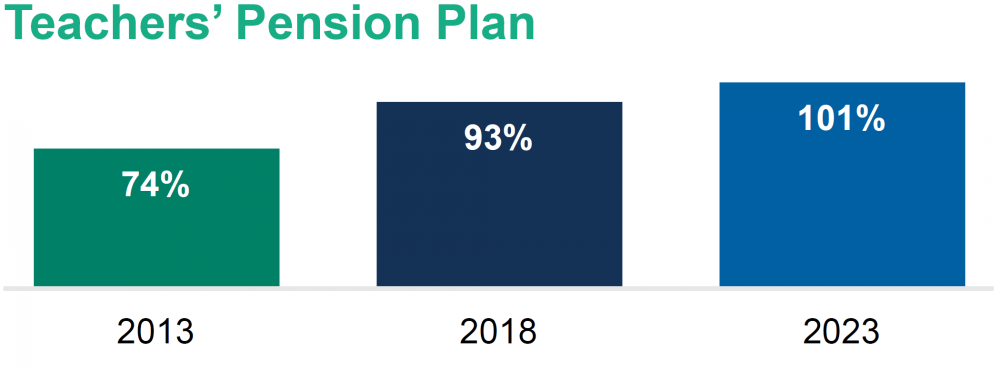

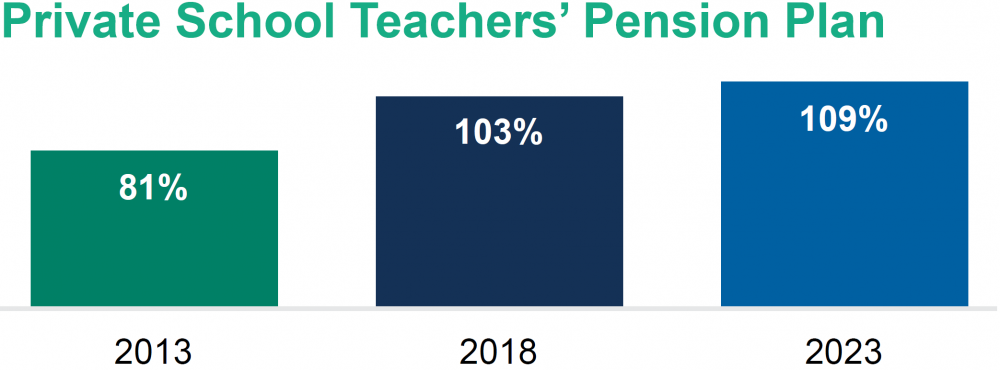

The Teachers’ Pension Plan is fully funded this year for the first time in its history: 101% funded ratio as at Aug. 31, 2023. The Private School Teachers’ Pension Plan remains fully funded with a funded ratio of 109%.

Funded Ratio

| . | $ Millions |

|---|---|

| Market Value of Assets | 22,755 |

| Fluctuation Reserve | 743 |

| Funding Value of Assets | 23,498 |

| Funding Liabilities | 23,237 |

| Funding Surplus (Deficit) | 261 |

| Funded Ratio | 101% |

| . | $ Millions |

|---|---|

| Market Value of Assets | 122.4 |

| Fluctuation Reserve | 4.0 |

| Funding Value of Assets | 126.4 |

| Funding Liabilities | 115.7 |

| Funding Surplus (Deficit) | 10.7 |

| Funded Ratio | 109% |

Plan Structure and Funding

The Teachers’ Pension Plan and the Private School Teachers’ Pension Plan have three unique funding arrangements and liability structures:

- Teachers’ Pension Plan pre-1992: A 2007 agreement between the Government of Alberta (GOA) and the ATA assigns government responsibility for liabilities associated with pensions for the period of service before September 1992.

- Teachers’ Pension Plan post-1992: The cost of pension benefits earned for service after August 1992 is shared between active plan members and the GOA. Funding deficiencies under the plan are amortized by additional contributions from active members and the Government of Alberta over a maximum 15-year period.

- Private School Teachers’ Pension Plan: In 1995, legislation established a separate plan for private school teachers. The funding of this plan mirrors the post-1992 portion of the Teachers’ Pension Plan, except the cost is shared between teachers and employers (private schools) instead of the Government of Alberta.

ATRF regularly conducts actuarial funding studies to assess the value of the plans’ liabilities compared to their assets and to ensure adequate funding. An actuarial valuation is a report on the health of the plans.

The plans’ funding is calculated using actuarial assumptions and methods. The funding assumptions include margins (or cushions) to buffer against unfavourable results in the rate of returns or other factors affecting the plans. The margin is one of the important risk management tools to help achieve our funding objectives of contribution stability and benefits being fully funded. Both plans have healthy margins built in at this time.

The funding valuation uses another tool to achieve our funding objectives. It’s an actuarially accepted practice of smoothing fund returns over a five-year period to even out the impact of the volatility of market returns on the plan’s funded status and contribution rates, acting as a powerful risk management lever. This practice produces a funding value of assets that can be higher or lower than the market value in any given year. The difference between the market value of assets and the funding value of assets is referred to as the fluctuation reserve.